The FDI That Hollows Out

June 2026 | Monthly Insights

How China’s Overcapacity Reaches Southeast Asia — and Why the Distress Hides From the Aggregates

Southeast Asia is being cast as the clear winner of the realignment of global manufacturing. As United States tariffs push capital out of China, the region is attracting billions of dollars of electric-vehicle and battery investment — BYD’s roughly US$900 million plant in Rayong, a multi-billion-dollar battery complex breaking ground in Karawang, and Chinese groups accounting for close to two-fifths of approved foreign-investment applications in Thailand by one measure. The story is real. It is also incomplete: the same overcapacity driving the investment is arriving simultaneously as an import flood that is hollowing out the region’s incumbent manufacturers — and the distress is concentrated precisely where the headline numbers cannot see it.

The Story the Region Is Telling Itself

Take the bull case at its strongest. Chinese capital is flowing into Southeast Asian manufacturing at scale: BYD opened a ~US$900 million plant in Rayong in mid-2024 with capacity for up to 150,000 vehicles a year; battery makers have followed, with a major cell investment among Thailand’s 2025 promotion applications and a ~US$6 billion battery plant breaking ground in Karawang, Indonesia. China is now among the largest sources of investment into Thailand — close to 40% of approved applications since early 2025 by one measure, and a top-three source by committed value alongside Singapore and Hong Kong, which themselves channel Chinese capital. The logic is impeccable: zero tariffs under the ASEAN–China Free Trade Agreement, proximity to vehicle assembly, and, in Indonesia’s case, the nickel reserves that anchor the battery supply chain.

The Flood Underneath the Investment

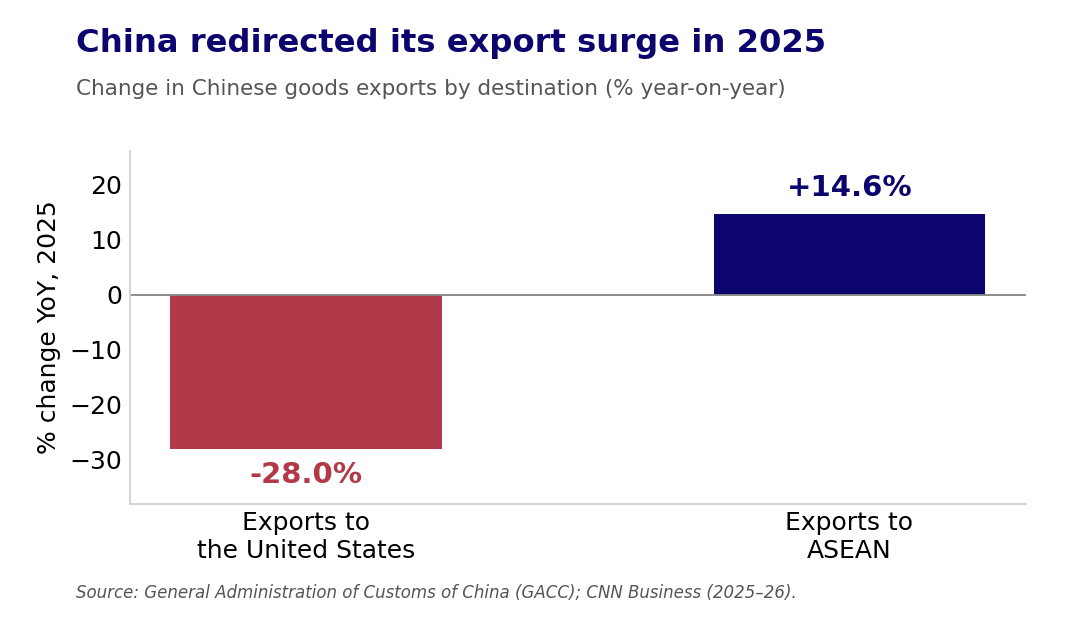

The discomfort begins with why the capital is moving at all: China cannot absorb its own output. Its customs administration reported a record US$1.19 trillion goods trade surplus in 2025 — the first time any economy has run a surplus above a trillion dollars. With shipments to the United States down around 28% under tariffs, that output was redirected; China’s exports to ASEAN rose 14.6%. Investment and imports are two faces of the same phenomenon: some overcapacity arrives as a factory and counts as inbound FDI, while much more arrives as goods that compete directly with what local factories already make. ASEAN’s goods trade deficit with China has widened to over US$180 billion, from roughly US$100 billion before the pandemic. The capital and the goods travel together; only one of them appears in the celebratory headlines.

Where the Incumbents Are Breaking

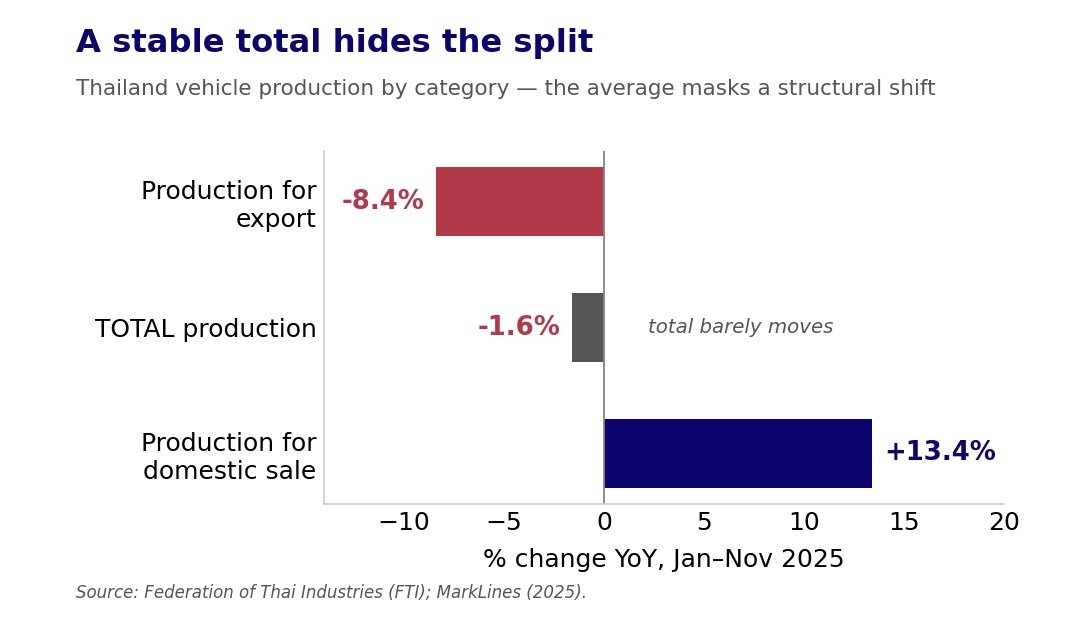

The clearest front line is automotive, and Thailand — long the region’s vehicle-manufacturing hub — is where it shows, though not in the way a headline would suggest. Per the Federation of Thai Industries, total vehicle production fell only ~1.6% over the first eleven months of 2025; beneath that, production for export dropped ~8.4% while domestic production rose ~13.4% and domestic battery-EV output surged more than sixfold as local-production rules took effect. The hub is not shrinking so much as changing hands: the export-oriented, internal-combustion base is contracting while Chinese-led EV assembly grows. On FTI registration data, Chinese brands have risen from ~4% of the Thai car market in 2021 to ~22.6% in 2025.

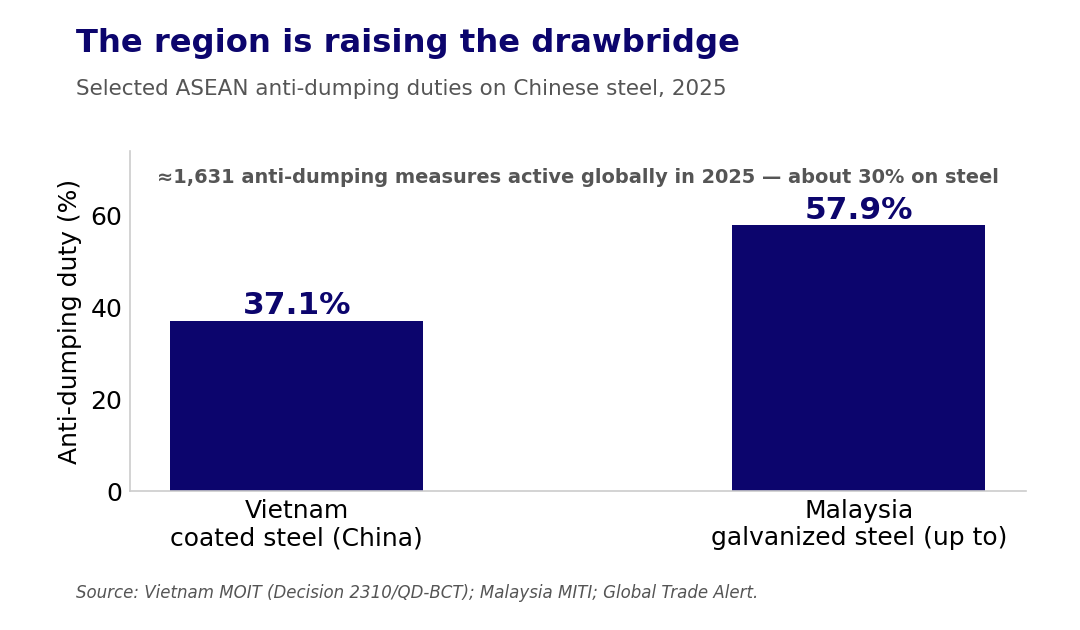

The incumbents are exiting the segment they once dominated: Subaru ceased Thai production at the end of 2024 and Suzuki will do so by the end of 2025, while Nissan is consolidating rather than closing. The detail that should most concern lenders is that the new investment does not rescue the old supplier base — Chinese original-equipment manufacturers run vertically integrated supply chains and source limited local content, so an EV plant arriving does not absorb the internal-combustion-era parts makers it renders obsolete. The pattern extends well beyond cars. Kasikorn Research Center counts roughly 4,302 Thai factory closures in 2023–24, concentrated in furniture, electronics, garments, automotive and steel; in Indonesia, the Manpower Ministry has projected textile-sector layoffs rising from around 80,000 in 2024 toward 280,000, with the bankruptcy of Sritex alone causing some 11,000 job losses. The policy reflex confirms the pressure: Vietnam has imposed definitive anti-dumping duties of up to 37.13% on Chinese coated steel and Malaysia provisional duties of up to 57.9% on galvanized steel, part of roughly 1,631 anti-dumping measures active worldwide in 2025.

An assembly plant changing owners is not the same as an industrial base staying healthy. The jobs, suppliers and tax base attached to the displaced capacity do not transfer to the vertically integrated entrant one-for-one. The headline “ASEAN wins manufacturing FDI” and the reality “incumbent manufacturers are being hollowed out” are both true at once.

Why the Aggregates Hide It

This is why so few boards have acted: the damage is largely invisible at the level most decision-makers monitor. Thailand’s manufacturing PMI read 52.7 in April 2026, according to S&P Global — expansion, and a twelfth consecutive month of it — while national FDI is at record highs. On those two numbers alone, a board could reasonably conclude that nothing is wrong. The numbers are not lying; they are averaging. New EV and battery output and resilient sub-sectors lift the index even as legacy producers contract beneath it. What the aggregates cannot show is composition: the mean holds steady while the distribution pulls apart, with concentrated casualties at one end. This is not a regional collapse — it is a reallocation with concentrated losers, which is precisely why it is missed, and why only a portfolio- or sector-level view can see it.

The Credit Dimension: Why “Non-Sponsored” Is Not “Safe”

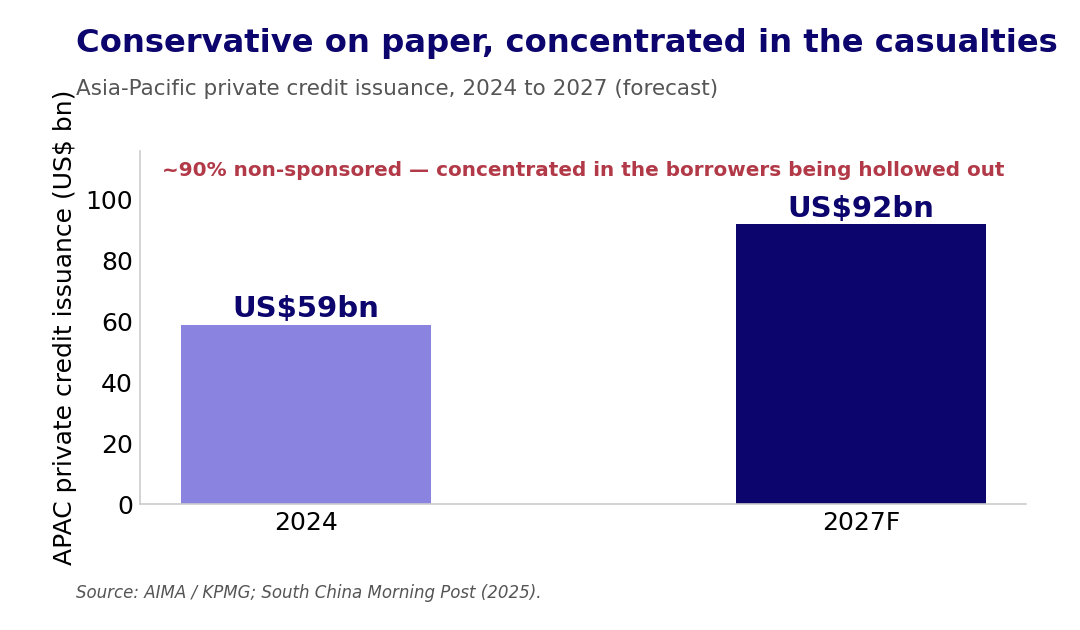

For lenders, the industrial story translates into asset quality. The pressure on incumbent manufacturers is structural, not cyclical — a competitor with a different cost base and a captive supply chain means margin compression that does not reverse when the cycle turns. The Asian Development Bank notes regional non-performing loans fell in 2024 but are projected to rise through 2027 on mounting credit stress, consistent with the lag between factory-floor pressure and recognised loan losses. Southeast Asian private credit deserves particular attention, because it is often described as structurally safer than its US counterpart. The US direct-lending market is dominated by sponsored, private-equity-backed, highly leveraged borrowers; the Southeast Asian market is roughly 90% non-sponsored, asset-backed lending to independent businesses, in a region where banks still supply the large majority of credit. On a US risk template, that looks conservative.

But the regional book is concentrated in exactly the domestic manufacturing and mid-market borrowers on the losing side of the reallocation — the furniture, garment, parts and steel businesses absorbing the import flood. Concentration in that base can make a non-sponsored book as risky as, or riskier than, a sponsored one. There is no private-equity sponsor standing behind the borrower to inject rescue equity or run a professional workout; the counterparty is a family enterprise whose own wealth is correlated with the failing business. And the comfort lenders draw from personal or family guarantees is largely illusory in a sector-wide downturn: a personal guarantee is only as good as the guarantor’s unencumbered, uncorrelated net worth, and when an entire sector is being hollowed out, the founder’s other assets are impaired at the same moment the guarantee is called. “Non-sponsored but personally guaranteed” is not a synonym for “safe”; it is a different risk, and in a correlated structural downturn, often a worse one.

What Good Looks Like

The argument is not against Southeast Asian manufacturing exposure — the region may yet be a net winner from the realignment. It is that “the region wins” and “your asset or borrower wins” are different propositions. For management and boards of exposed incumbents, the durable options are to reposition into segments the entrant does not want — specialised components, aftermarket, services — or to convert the competitor into a counterparty through a joint venture or supply agreement on clear terms, rather than competing head-on on price; where a franchise is structurally impaired, an early, deliberate restructuring preserves more value than a slow defence. For lenders, the imperative is to re-underwrite manufacturing exposure against the reallocation rather than aggregate sector health, to stress collateral and guarantees for a correlated downturn, and to engage borrowers while options still exist.

The investment into Southeast Asian manufacturing is real, and so is the hollowing-out. They are produced by the same force, and they fall on different balance sheets. The averages — PMI, headline FDI — will continue to look benign for some time, because they are measuring a market in which winners and losers are netting out. The institutions that act while the aggregates still look healthy will have the widest set of choices; those that wait for the data to confirm the problem will be restructuring, not repositioning. The task is to know which side of the reallocation you are on — before the averages catch up with you.