Defensive Does Not Mean Simple: What Investors Miss in Real Asset Diligence

May 2026 | Monthly Insights

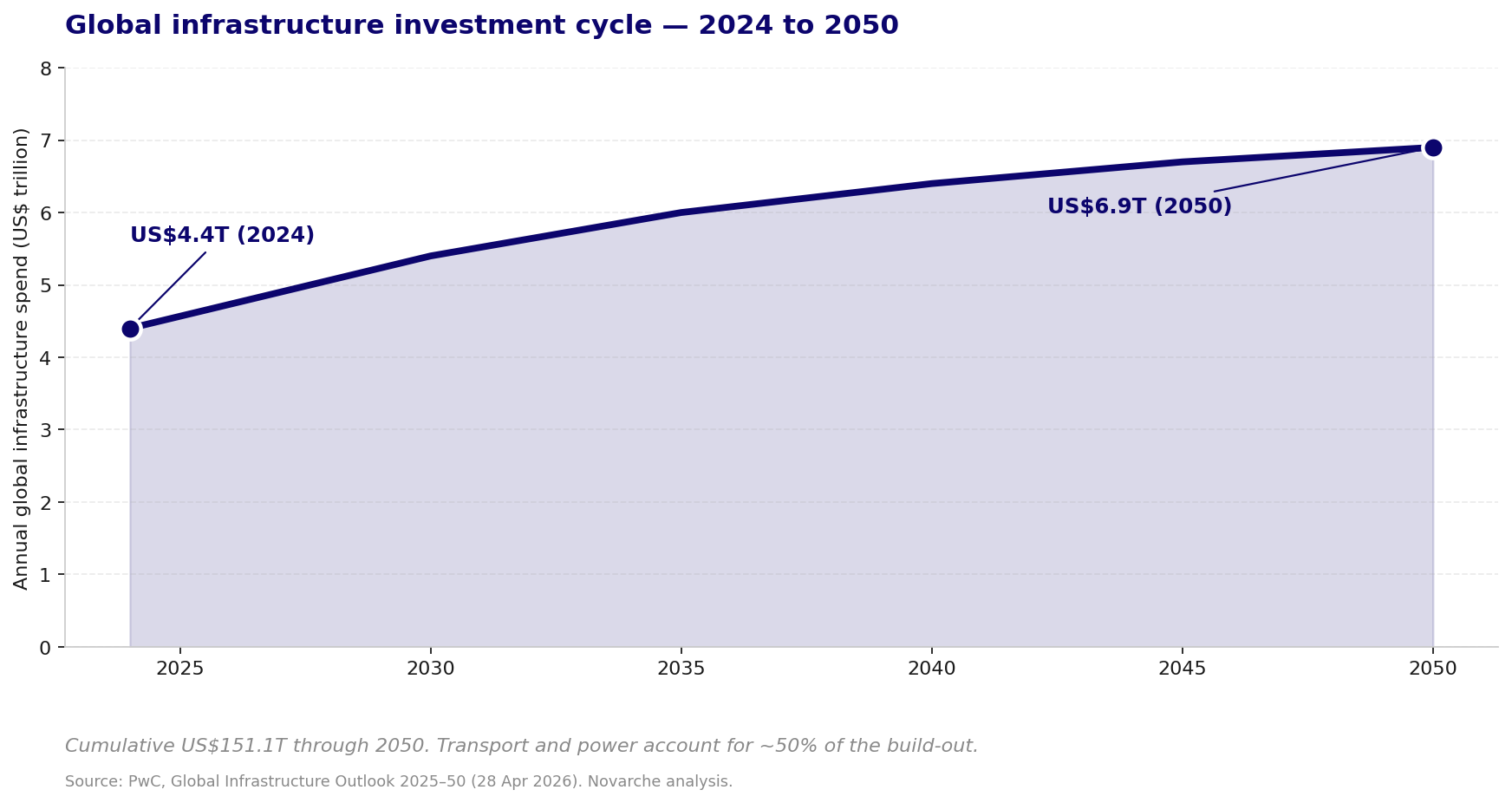

Capital is rotating back into real assets — but not just into real estate. APAC commercial real estate volumes hit US$47.0 billion in Q1 2026, up 31% year-on-year and the strongest first quarter on record. PwC forecasts global infrastructure spending will rise from US$4.4 trillion to US$6.9 trillion annually by 2050. APAC private credit is on track to grow from US$59 billion to US$92 billion by 2027 — the fastest growth rate of any region. The category, in short, is being unbundled. The diligence question is no longer whether an asset is defensive. The better question is what makes the cash flow defensible — and under what conditions could that change.

The Rotation Back to Real Assets

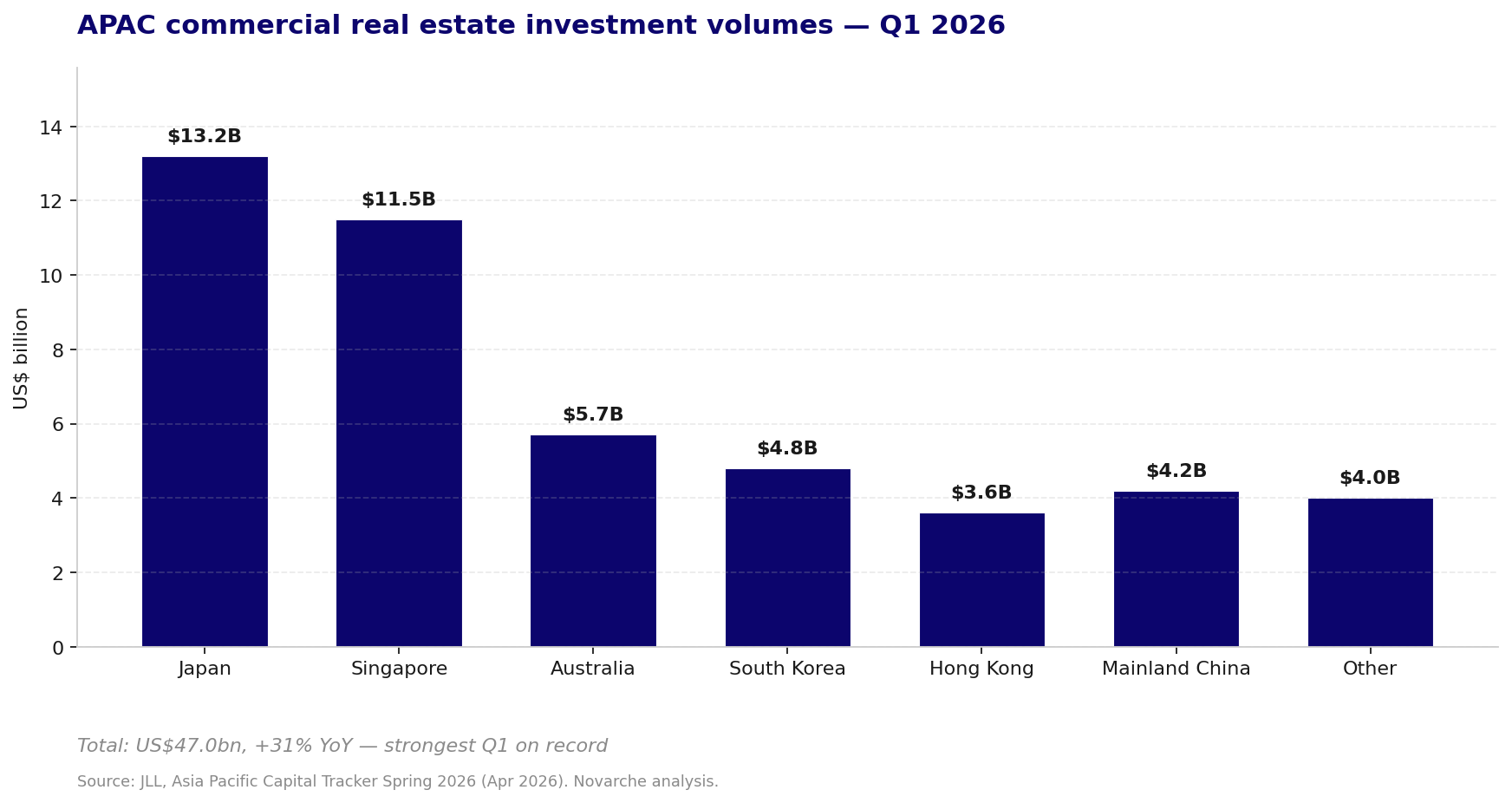

JLL's APAC Capital Tracker reports Q1 2026 volumes of US$47.0 billion (+31% YoY). Japan led at US$13.2 billion despite a 4% YoY decline; Singapore followed with US$11.5 billion driven by a mega-fund and portfolio acquisitions; Australia recorded US$5.7 billion (+49% YoY). CBRE's 2026 Asia Pacific Investor Intentions Survey, based on 420+ investor responses, shows net buying intentions improving from 5% in 2024 to 13% in 2025 and 17% in 2026 — the highest reading in four years.

Two features of this rotation deserve more attention than the headline. First, dispersion: REITs have moved to net buying intentions of +30%, while private investors flipped to -3% — the first negative reading in five years. Second, re-segmentation: the office sector has overtaken industrial and logistics as APAC's most preferred real-estate asset class for the first time in six years. And within the broader real-assets bucket, infrastructure and private credit are pulling capital away from real estate. Per MSCI's Real Assets in Focus 2026, real estate target allocations fell for the first time in 13 years in 2025, and roughly 60% of investors now treat infrastructure and private credit as direct competitors to real estate.

The Trap in the Word "Defensive"

Real assets are often described as defensive because they are linked to essential services, real-economy demand, contracted revenue or physical collateral. The description is directionally useful but it can hide the actual risk. Defensive demand does not automatically create defensive cash flow — and the architecture of contracts, operations, regulation, capex and financing is what determines durability. The trap is most visible when you walk through each of the five mainstream real-asset categories.

Transport Infrastructure: Structural Need ≠ Execution

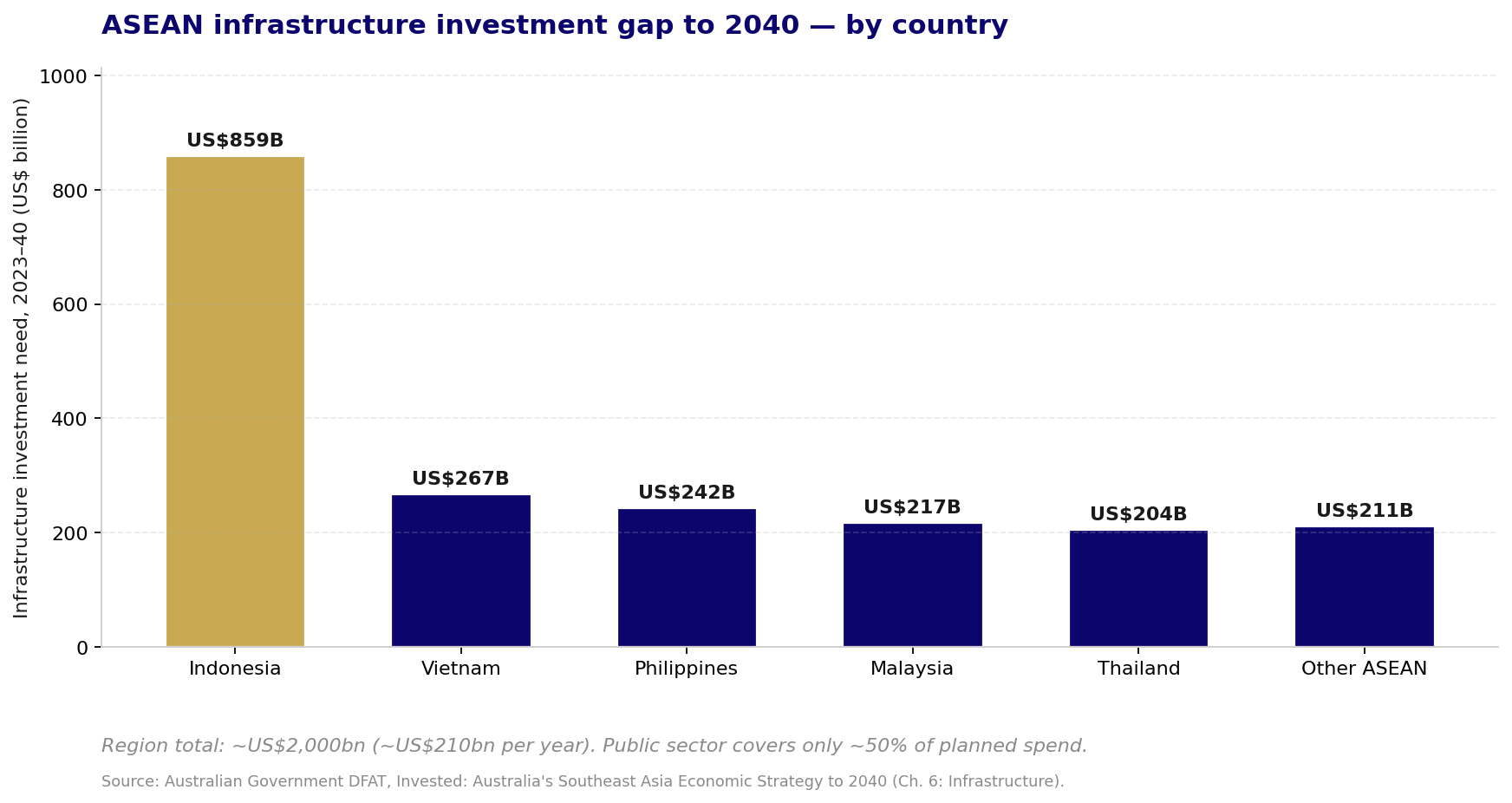

PwC's Global Infrastructure Outlook 2025–50 forecasts that transport and power together will absorb roughly US$75 trillion of the US$151.1 trillion cumulative spend through 2050. In Southeast Asia, the Australian Government's Invested strategy estimates a US$3 trillion infrastructure investment gap to 2040 — averaging around US$210 billion per year — with Indonesia accounting for US$859 billion of that need, Vietnam US$267 billion, the Philippines US$242 billion, Malaysia US$217 billion and Thailand US$204 billion.

The execution path is harder than the demand curve suggests. ACI Asia-Pacific & Middle East projects roughly US$240 billion of airport capex across the region between 2025 and 2035 — US$136 billion to modernise, US$104 billion for greenfield builds — with major ASEAN projects including Vietnam's Long Thanh, Bangkok-Suvarnabhumi expansion and the NAIA PPP. The constraint is not need; it is bankable structure. Concession assets are only as defensive as the concession terms, traffic forecasts, step-in rights and maintenance obligations they sit on.

Energy and Utilities: Regulated Revenue, Transition Risk

Energy and utilities are the textbook defensive real asset — long-dated, regulated, often inflation-linked. They are also the category where regulatory rules are being rewritten fastest, which means assets in underwriting today are being priced against a moving target.

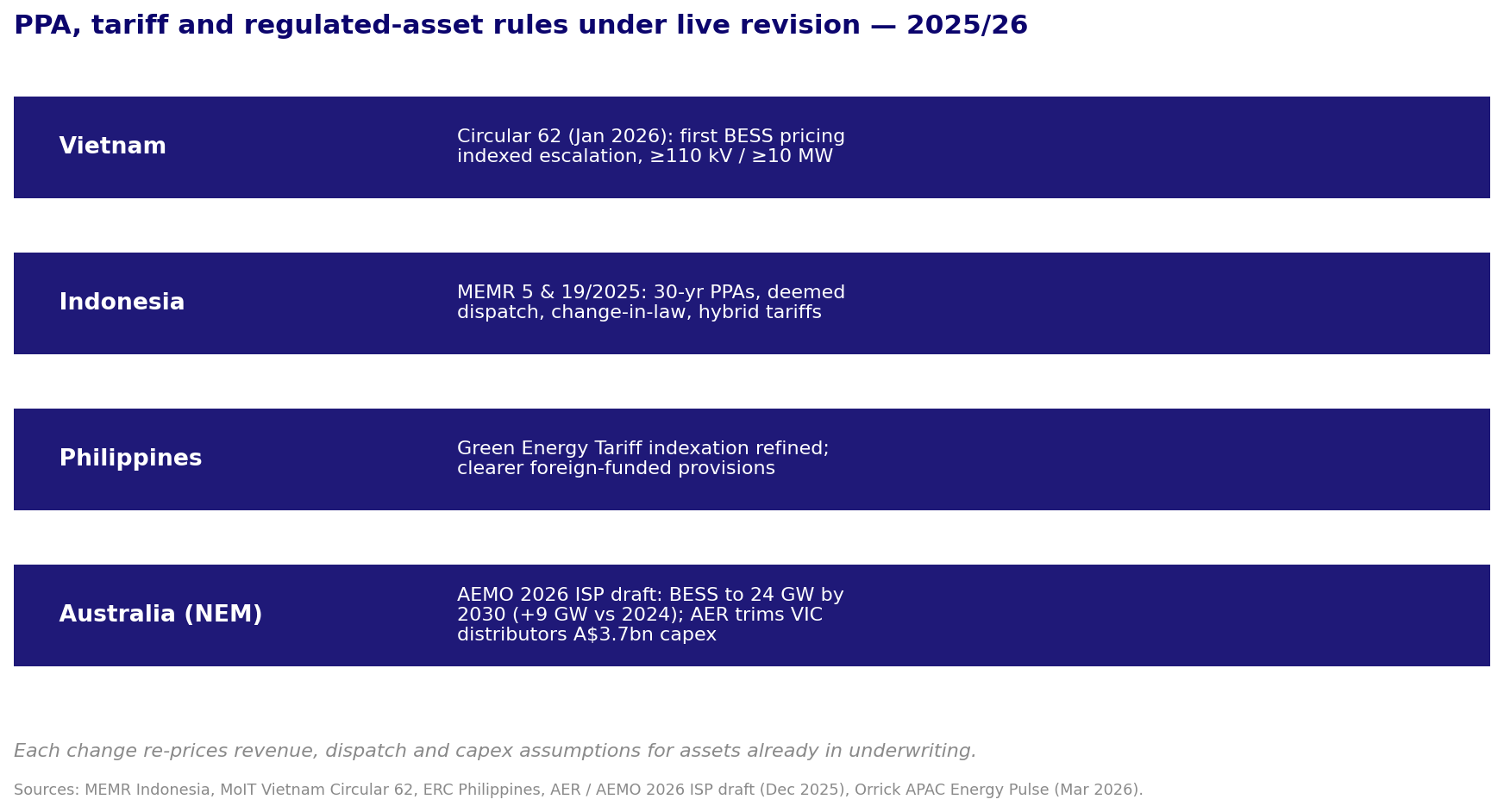

Vietnam's Circular 62/2025, effective 26 January 2026, introduces the country's first BESS pricing framework — a two-part tariff with capacity and energy components plus foreign-exchange adjustment — for projects ≥110 kV and ≥10 MW. Indonesia's MEMR Regulation 5/2025 codifies a new renewable PPA framework, replacing MEMR 10/2017, that allows PPA terms to extend beyond 30 years, entitles independent power producers to deemed-dispatch payments where PLN curtails, and clarifies network-reliability obligations. MEMR Regulation 19/2025 (29 December 2025) creates a hybrid power plants framework that formally embeds battery storage as a system component. In Australia, AEMO's draft 2026 Integrated System Plan was analysed by Modo Energy as raising grid-scale battery storage to 24 GW by 2030 — around 9 GW above the 2024 ISP — while the Australian Energy Regulator trimmed Victorian distributors' proposed capex by A$3.7 billion for the 2026–31 regulatory period. Each of these moves re-prices revenue, dispatch, capex or regulated asset base.

Digital Infrastructure: Visible Demand, Constrained Delivery

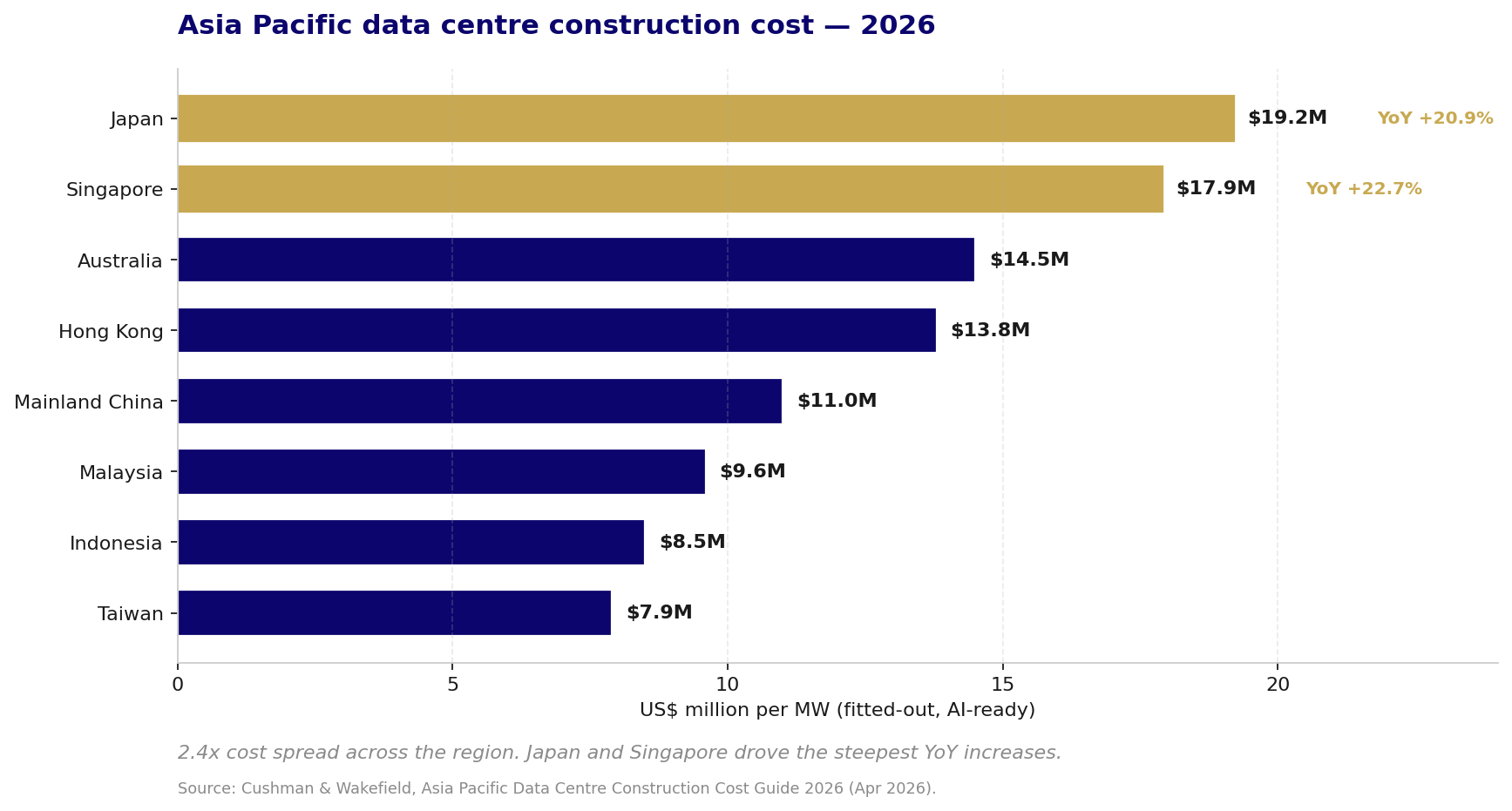

Cushman & Wakefield's 2026 APAC Data Centre Construction Cost Guide reports build costs ranging from US$7.9 million per MW in Taiwan to US$19.2 million in Japan and US$17.9 million in Singapore — a 2.4x spread. Year-on-year, Japan rose 20.9% and Singapore 22.7%, the steepest increases among the largest hubs.

Power is the gating item. Singapore's 2023 pilot Data Centre Call for Application allocated only 80 MW; the second round (DC-CFA2), launched 1 December 2025, makes 200 MW available with a stricter sustainability bar — Green Mark Platinum, PUE ≤ 1.25, ≥50% green-energy supply. The IEA projects global data-centre electricity demand will exceed 1,000 TWh by 2026 — equivalent to Japan's annual electricity consumption. AI-ready facilities also demand higher power density, advanced cooling and different structural specs. The risk is not that demand disappears. It is that demand is real but the asset cannot deliver capacity at the cost, timing or technical specification assumed in the model.

Logistics and Industrial Real Estate: Tight Prime, Brittle Stock

Cushman & Wakefield's Q1 2026 Singapore Industrial MarketBeat reports prime logistics rents rose 1.5% quarter-on-quarter — the strongest quarterly growth since Q1 2024 — while warehouse vacancy fell to 5.6% and new supply is set to fall below 10-year averages in 2026. CBRE flags a parallel risk: oil-price spikes and elevated transport costs could dampen demand even where leasing has held firm. The implication is that 'logistics exposure' is not enough. Investors need to distinguish between prime, automation-ready, well-located facilities and older stock that may face vacancy, ESG, loading, ceiling-height or layout obsolescence. Location and operating efficiency now matter more than the asset-class label.

Credit on Real Assets: Asset-Backed ≠ Protected

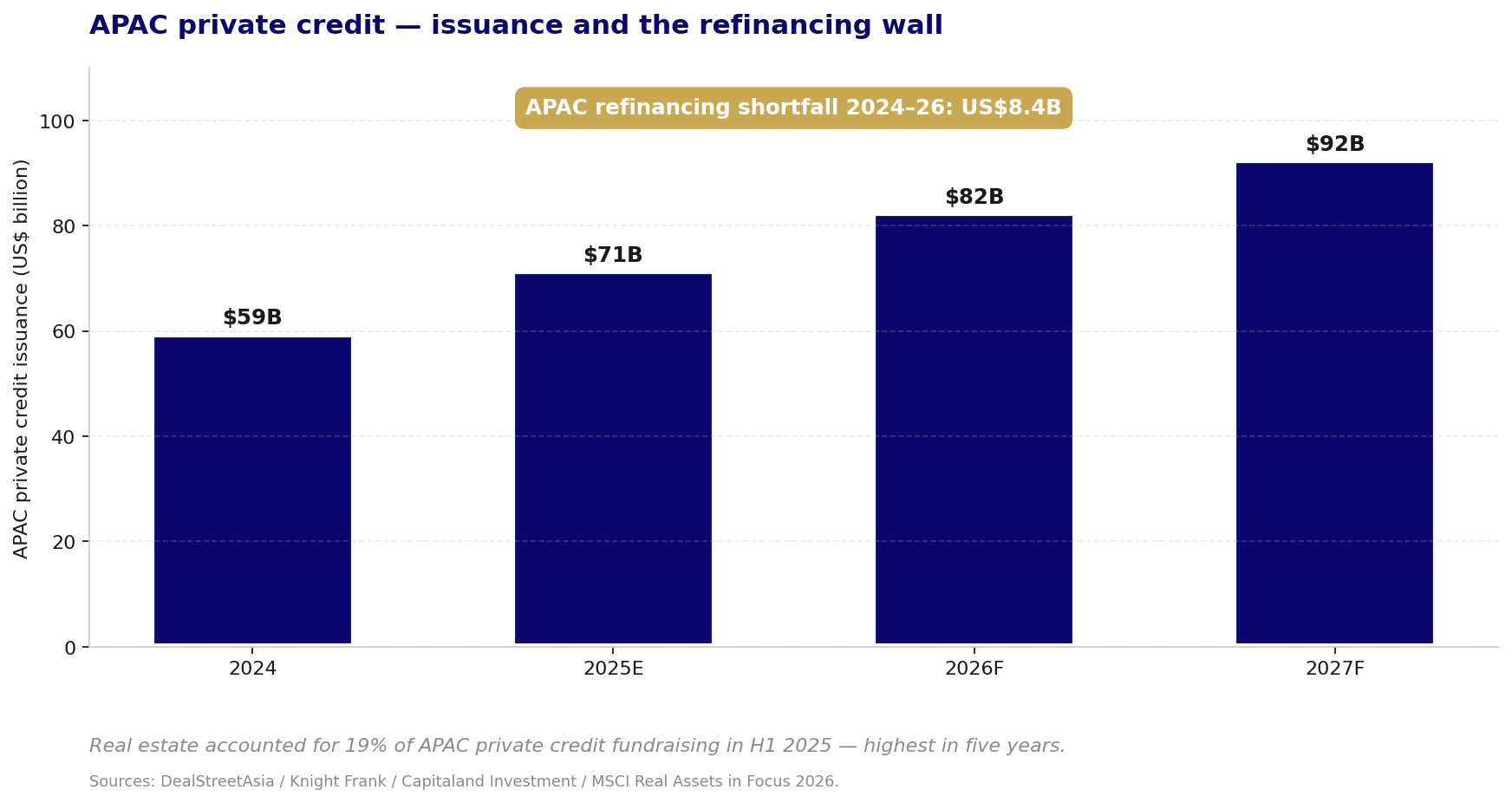

Per AIMA / KPMG, APAC private credit issuance is on track to rise from US$59 billion in 2024 to US$92 billion by 2027 — a 16% CAGR, faster than any other region. Knight Frank reports real estate accounted for 19% of APAC private credit fundraising in H1 2025 — the highest share in five years — with Australia (40%) and India (36%) leading regional activity.

CBRE estimates the APAC commercial real estate refinancing shortfall at US$8.4 billion over 2024–2026, with Australia (US$4.6 billion) and mainland China (US$2.9 billion) accounting for the bulk; refinancing costs in Australia and Hong Kong could be up to 1.9 times higher over the next two years. For lenders, the diligence test is not loan-to-value at origination. It is whether the valuation is realisable under stress, whether enforcement is practical in the relevant jurisdiction, whether a refinancing market exists at maturity, and whether the sponsor has both the willingness and the capacity to support the asset if the base case slips.

The Risks Boards Are Not Pricing

Three risk vectors recur across every real-asset category. They are not new in isolation, but they now interact in ways conventional underwriting frameworks were not built to capture:

· Power, capex and the cost spread. The 2.4x spread in DC build cost changes yield-on-cost, debt sizing and exit valuation. The same dynamic — capex inflation outrunning underwriting assumptions — is now visible in regulated utilities (AEMO's +9 GW BESS uplift in a single planning cycle), in transport infrastructure (airport budgets revised upward) and in logistics (ESG and automation retrofit). Capex inflation is now a category-wide variable, not a digital-infrastructure issue.

· Trade policy risk. On 11 March 2026, USTR launched Section 301 investigations against 16 economies — including six in ASEAN: Singapore, Indonesia, Malaysia, Cambodia, Thailand and Vietnam — citing structural excess capacity. The Section 122 global tariff (set at 10% on 24 February 2026) expires on 24 July 2026 (the 150-day statutory cap, unless Congress extends), and a USTR public hearing is scheduled for 5 May 2026. For port-adjacent transport infrastructure, manufacturing-linked logistics, and any infra asset whose covenant depends on US export flows, trade policy is now a tenant-credit variable.

· The refinancing wall. APAC's US$8.4 billion CRE refinancing shortfall is small in absolute terms versus Europe (US$191.4 billion) and the US (US$157.3 billion), but concentrated in Australia and mainland China. Private credit is filling some of the gap, but each Southeast Asian jurisdiction has distinct enforcement law, creditor protections and legal infrastructure. Underwriting on a single regional template will price the risk wrong.

None of these risks are individually catastrophic. Their danger lies in their interaction. An investor that has bought logistics exposure to capture supply-chain diversification benefits, financed with floating-rate debt, leased to manufacturers exporting to the US, and located in a power-stressed industrial estate, is exposed to all three vectors at once. The headline yield will look attractive. The covariance of risk across the underwriting will not.

What Good Looks Like

The opportunity is real, and visible cash flows do deserve a premium in volatile markets. The argument is that the diligence discipline required to capture that opportunity has not kept pace with the speed at which capital is flowing into the asset class. We see five areas where the gap between commercial conviction and underwriting discipline is widest:

· Sector framing. Cash-flow architecture diligenced asset by asset, irrespective of label or sector — not defensive vs cyclical labels at the asset-class level.

· Power and capex. Stress-tested capex curves with sensitivity to grid-access timeline, ISP / RAB revisions and AI-density retrofit — not DCF on assumed industry-standard build costs.

· Trade exposure. Bilateral tariff scenarios mapped to tenant volumes, margins and contract enforcement across the holding period — not tenant covenant checks at point of underwriting.

· Credit underwriting. Realisable valuation under enforcement and a refinancing-market test at maturity, in the relevant jurisdiction — not loan-to-value at origination as the headline metric.

· IC discipline. One reconciled underwriting view of how cash gets interrupted, who controls the downside, and what capital protects value — not financial, legal, technical and regulatory workstreams reviewed in parallel.

These are not abstract recommendations. They reflect the operational reality of advising corporates and investors navigating real-asset allocation today. The cost of building this discipline is modest relative to the cost of discovering, under pressure, that it was not built.

Conclusion

Real assets are back in focus because the macro environment has made visible cash flows more valuable. But visibility is not certainty, and asset backing is not downside protection.

The most attractive real assets are not necessarily those with the strongest sector narrative. They are those where the cash-flow drivers have been properly tested: who pays, under what contract, under which regulation, with what capex, at what financing cost, and with what remedies if the base case fails.

Transport infrastructure, energy and utilities, digital infrastructure, logistics and industrial real estate, and credit on real assets can all be defensive. They can also be complex, capital-intensive and exposed to risks that conventional investment memos understate. The danger in the current market is not that investors ignore real assets. It is that they overpay for the appearance of defensiveness without diligence on the conditions that make the cash flow resilient.