The Monitoring Agent Paradox: Value Destruction in the Name of Oversight

March 2026 | Monthly Insights

The post-restructuring monitoring agent has become one of the least scrutinised features of modern workout transactions. Our analysis suggests these appointments persist more from institutional convention than demonstrated outcomes, even as technology has materially reduced informational asymmetry.

What Are Monitoring Agents?

Monitoring agents are independent accountants or financial advisors appointed by lenders to oversee borrower compliance following a restructuring. Unlike Chief Restructuring Officers who assume operational control, or lenders' internal credit teams who monitor from a distance, monitoring agents occupy a middle ground—they verify financial information, validate covenant calculations, and report compliance status to lenders on an ongoing basis.

The appointment typically follows a completed workout, debt restructuring, or forbearance agreement. Having negotiated new terms, reduced debt burdens, and imposed stricter covenants, lenders require independent verification that the restructured company adheres to its commitments. The monitoring agent becomes the lender's eyes and ears inside the business—without the authority to make decisions, but with unfettered access to financial data.

These arrangements do not have predetermined end dates. While initial restructuring agreements may specify an initial monitoring period, monitoring frequently continues as long as the restructured debt remains outstanding. In practice, this can persist for years.

The Evidence Gap

The fundamental premise underlying monitoring agent appointments is that independent third-party verification prevents fraud, detects covenant breaches early, and protects lender interests. This premise, however, rests on assertion rather than evidence.

After extensive research across industry publications, court filings, and academic databases, we find no publicly available statistics demonstrating that monitoring agents:

Detect covenant breaches faster than automated systems

Identify fraud that would otherwise go undetected

Improve post-restructuring performance outcomes

Reduce default rates compared to alternative oversight mechanisms

Private credit default rates have risen to 5.7% in early 2025, up sharply from the near-zero default environment of 2022. Broader loan defaults across all issuers averaged 4.3% versus pre-pandemic norms of 2–3%. These figures are macro indicators—not evidence for or against monitoring agents. Their relevance is operational: a higher-default environment increases the number of restructurings, which expands the population of post-restructured borrowers subject to monitoring requirements.

This raises the bar for monitoring effectiveness. The question is not whether monitoring can prevent market-wide defaults, but whether these mandates measurably improve post-restructuring outcomes—earlier detection of renewed deterioration, fewer repeat covenant breaches, reduced re-default incidence, and improved recoveries—versus technology-enabled continuous monitoring or direct lender oversight.

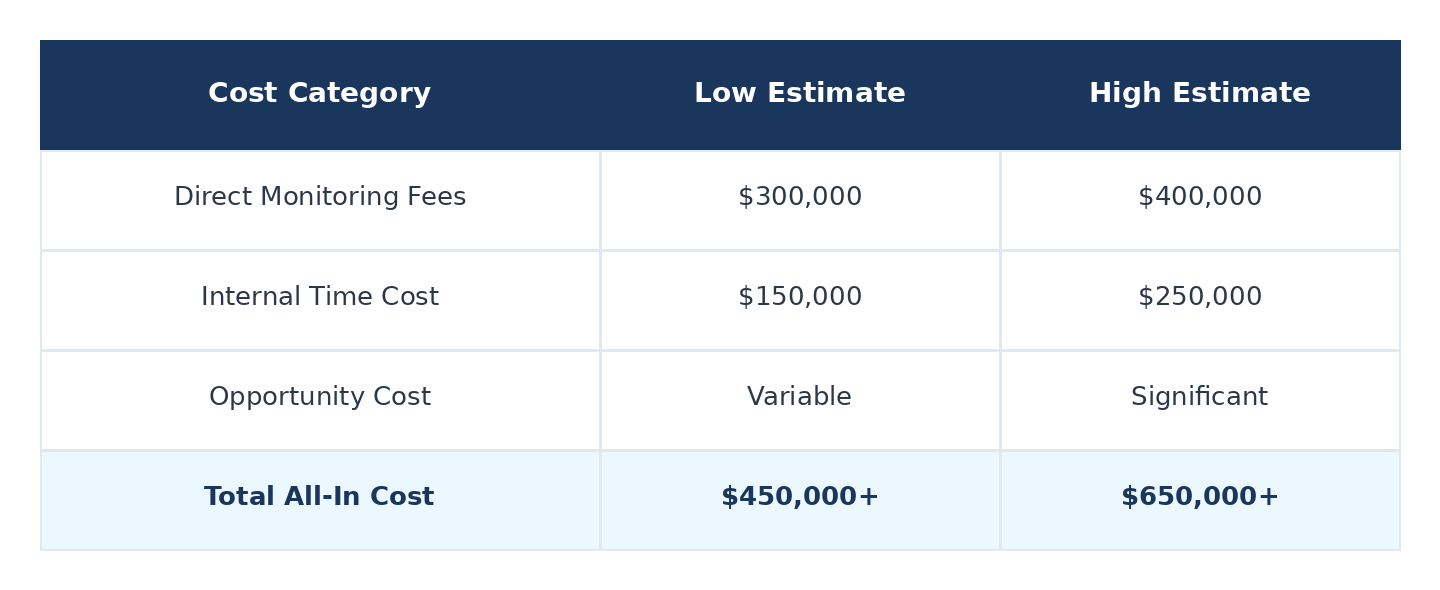

The Hidden Costs

Direct monitoring fees represent only the visible component of the cost structure. The operational burden on already-struggling companies creates a cascade of value destruction that can exceed the line-item expense.

Based on typical covenant reporting requirements, CFOs and finance teams often dedicate 40–60 hours per month to monitoring-related compliance—approximately 15–20% of senior finance team capacity consumed by compliance activities. These are hours not spent on cash optimisation, vendor negotiations, revenue initiatives, or operational efficiency improvements.

Trust Cost of Monitoring (Annual)

Perhaps most damaging is the decision paralysis induced by monitoring arrangements. Management teams, knowing that monitoring agents will scrutinise deviations from plan, may default to conservative strategies even when aggressive action is required. The friction of navigating approvals, preparing justifications, and managing lender expectations slows decision velocity when speed is essential.

Technology Has Changed the Game

The monitoring agent model emerged in an era when lenders lacked direct access to borrower financial data. That era has ended.

Today's covenant and portfolio monitoring systems can provide continuous visibility, faster exception detection, and forward-looking signals that periodic human review cannot match. Modern platforms deliver:

Real-time covenant tracking: Systems connect to borrower ERP and banking feeds, calculating covenant ratios as transactions post. Breaches and near-breaches can be flagged within hours rather than weeks.

AI-enabled anomaly detection: Algorithms identify unusual patterns—vendor concentration, invoice timing anomalies, working capital swings—that may not be evident in monthly reporting packages.

Automated dashboards and audit trails: Lenders access live views of covenant compliance, liquidity, and KPIs, reducing reliance on static reporting packs.

Predictive analytics: Stress scenarios and forward projections enable earlier intervention while operational options remain available.

This shift is not theoretical. Major institutions are embedding technology into monitoring workflows—deploying portfolio monitoring platforms, covenant tracking systems, and integrated data capture tools that provide continuous oversight across the credit lifecycle.

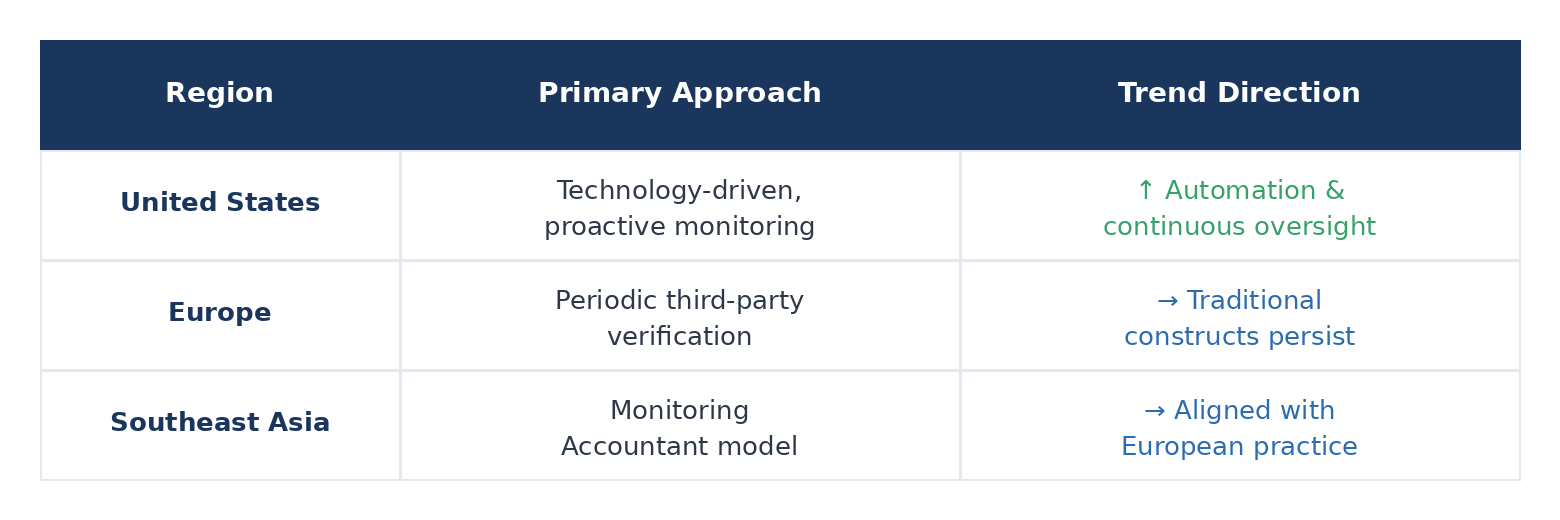

Divergence By Regions

The U.S. private credit market is increasingly moving monitoring upstream: tighter reporting standards at origination, automated covenant computation, centralised portfolio data capture, and early-warning triggers that prompt intervention while operational optionality remains.

This shift has been sharpened by several high-profile U.S. private credit failures that drew scrutiny to collateral integrity, governance, and transparency. These cases reinforce a core point: when information is late, disputed, or incomplete, post-event verification adds cost but does not reliably prevent value destruction.

By contrast, European markets remain more reliant on periodic third-party verification and traditional monitoring arrangements in restructured credits. Southeast Asia—especially Singapore—shows a similar pattern via the widespread "Monitoring Accountant" construct used by lenders after implementation of a restructuring plan.

Divergence - Comparison By Regions

The Agency Problem

The monitoring agent model suffers from structural conflicts. Monitoring agents are typically paid by the distressed company but serve lender interests. This creates an incentive misalignment that is rarely acknowledged but often felt in practice.

When uncertain, monitoring agents may default to flagging potential issues rather than exercising commercial judgment, creating false positives that consume management time and erode lender confidence unnecessarily. The incentive structure rewards demonstrating vigilance, not confirming stability.

Many monitoring agents come from firms that also provide restructuring advisory services, creating a revolving-door dynamic. In some cases, the same ecosystem that designs the restructuring framework later profits from monitoring it—blurring accountability for whether the plan was realistic, whether early signals were acted upon, and whether outcomes improved.

Without independent performance measurement, these agency problems persist unchallenged.

A Call to Action

Monitoring agents represent a market inefficiency: a practice that persists through institutional inertia and aligned incentives rather than demonstrated performance. The conditions that originally justified the model—genuine informational asymmetry and limited technology—have changed fundamentally.

Lenders should demand evidence. The next restructuring agreement that crosses your desk—scrutinise the monitoring provisions. Ask:

What specific, measurable value does the monitoring agent provide that technology platforms cannot?

Why are major institutions investing heavily in automated monitoring if periodic human review is superior?

Would those funds create more value invested in technology infrastructure or operational improvements with proven ROI?

The companies paying monitoring fees are the ones least able to afford services without demonstrated effectiveness. Every dollar diverted to unproven oversight is a dollar not invested in survival.

The technology exists. The alternative oversight models function. The only missing ingredient is the willingness to challenge an established practice that extracts value without proving outcomes.

The time to act is now—while restructured companies still have resources to invest in solutions that actually work.