The Connector Economy Trap: Strategic Risks Hidden in Southeast Asia's Growth Story

April 2026 | Monthly Insights

Southeast Asia’s growth narrative is compelling — and largely correct. But the speed at which capital is flowing into the region is outpacing the institutional infrastructure needed to absorb it. For boards and investors scaling operations across ASEAN, the question is no longer whether to be here. It is whether they are pricing the real risks of being here.

The Growth Story Everyone Knows

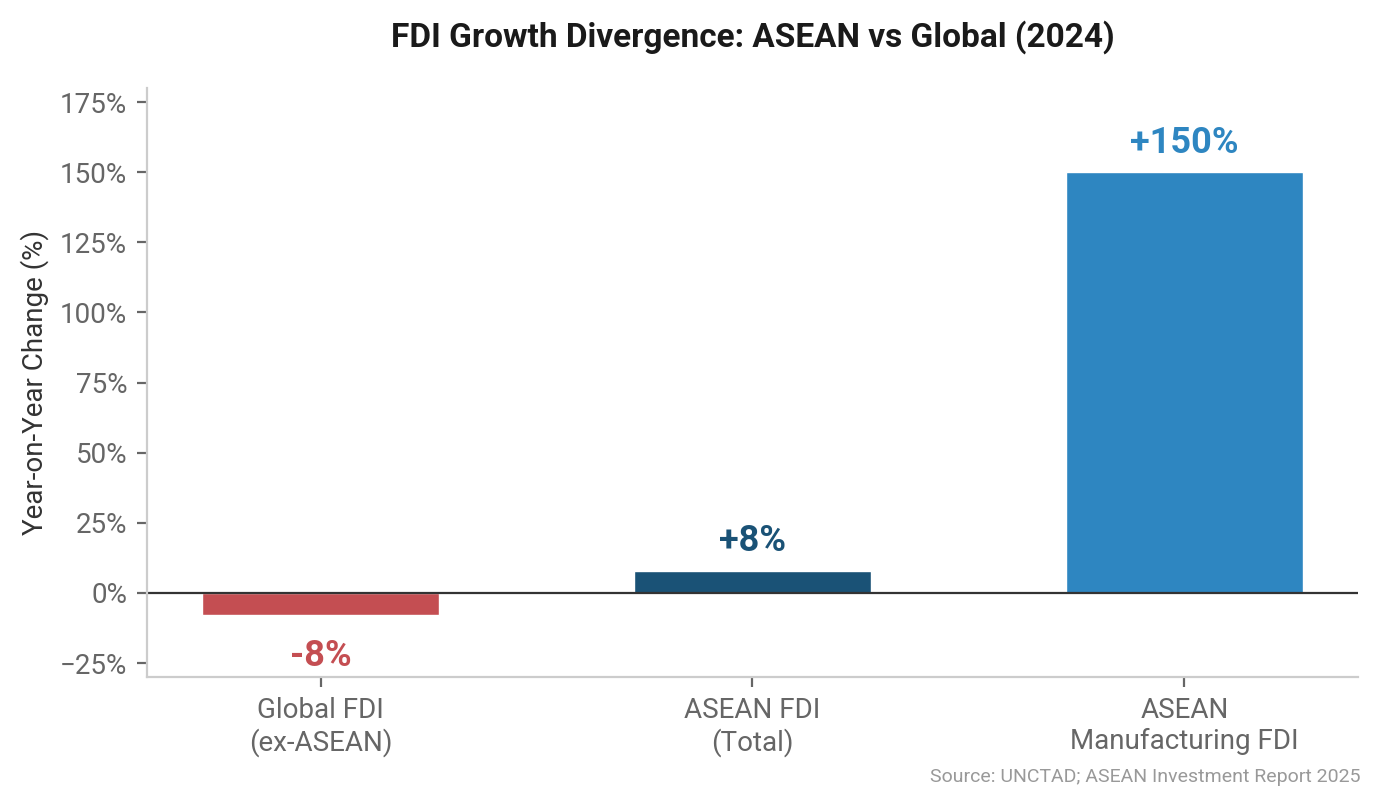

ASEAN attracted over $226 billion in foreign direct investment in 2024, defying a global decline of 8%. Manufacturing investment — the category most closely linked to supply chain repositioning away from China — surged approximately 150% to $44 billion. Vietnam’s economy grew 6.6% in 2025. The Asian Development Bank projects the region will grow 4.4% in 2026, with the Philippines and Indonesia at 5.3% and 5.0% respectively.

These numbers have attracted record capital, generated political goodwill, and established the region as a credible manufacturing alternative to China. What they do not tell is the story of how that capital is distributed, how dependent the region’s growth model is on a narrow set of trade corridors, or how prepared its institutions are for the governance demands that follow.

One Corridor, Two Masters

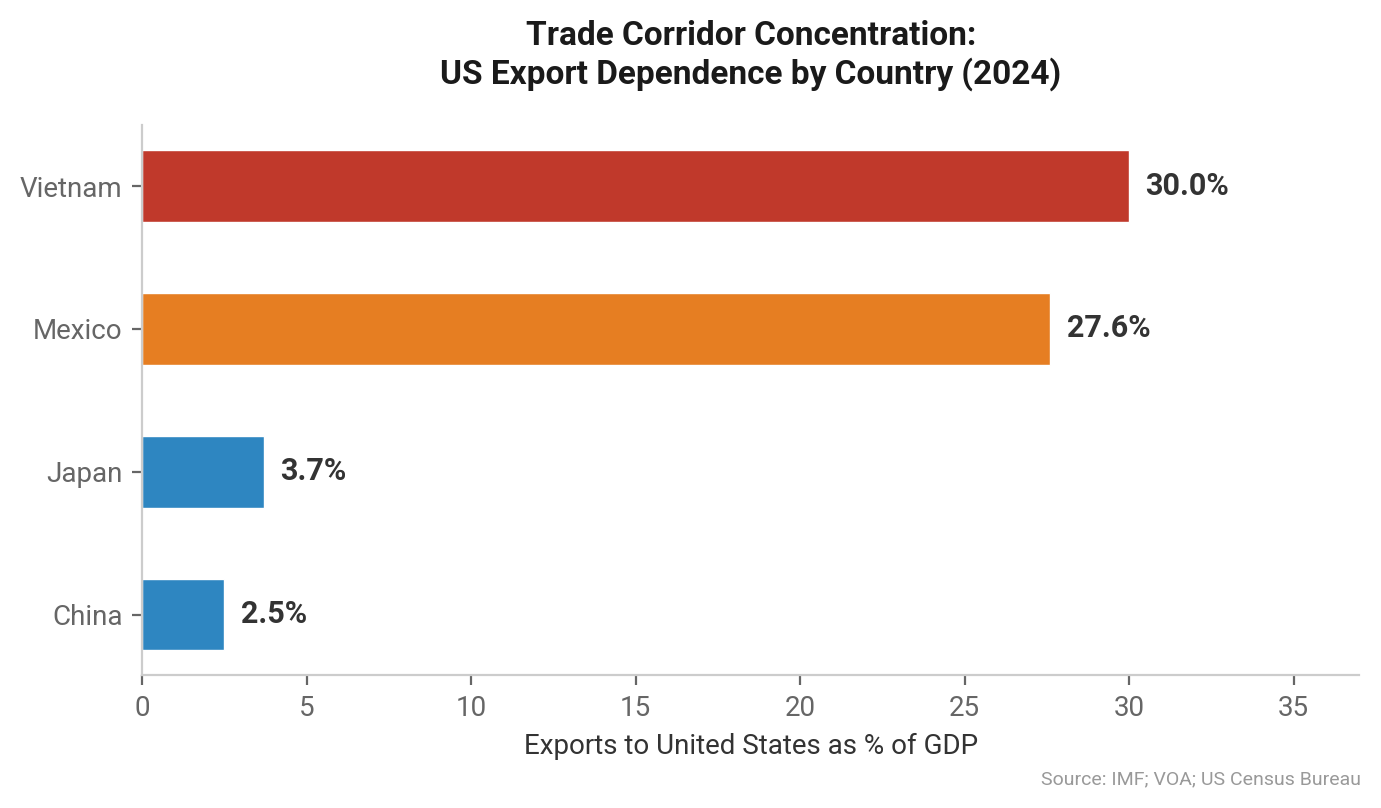

ASEAN’s role as a connector between the United States and China is frequently cited as a structural advantage. In practice, it is also a source of acute fragility.

Vietnam’s exports to the United States represent approximately 30% of its GDP — the highest ratio of any US trading partner. Mexico’s equivalent figure is 27.6%. China’s is just 2.5%. This concentration carries direct policy risk: in April 2025, the Trump administration imposed “reciprocal tariffs” of 19–20% across most ASEAN economies under IEEPA, with Vietnam initially facing a 46% rate.

The Legal Ground Shifts

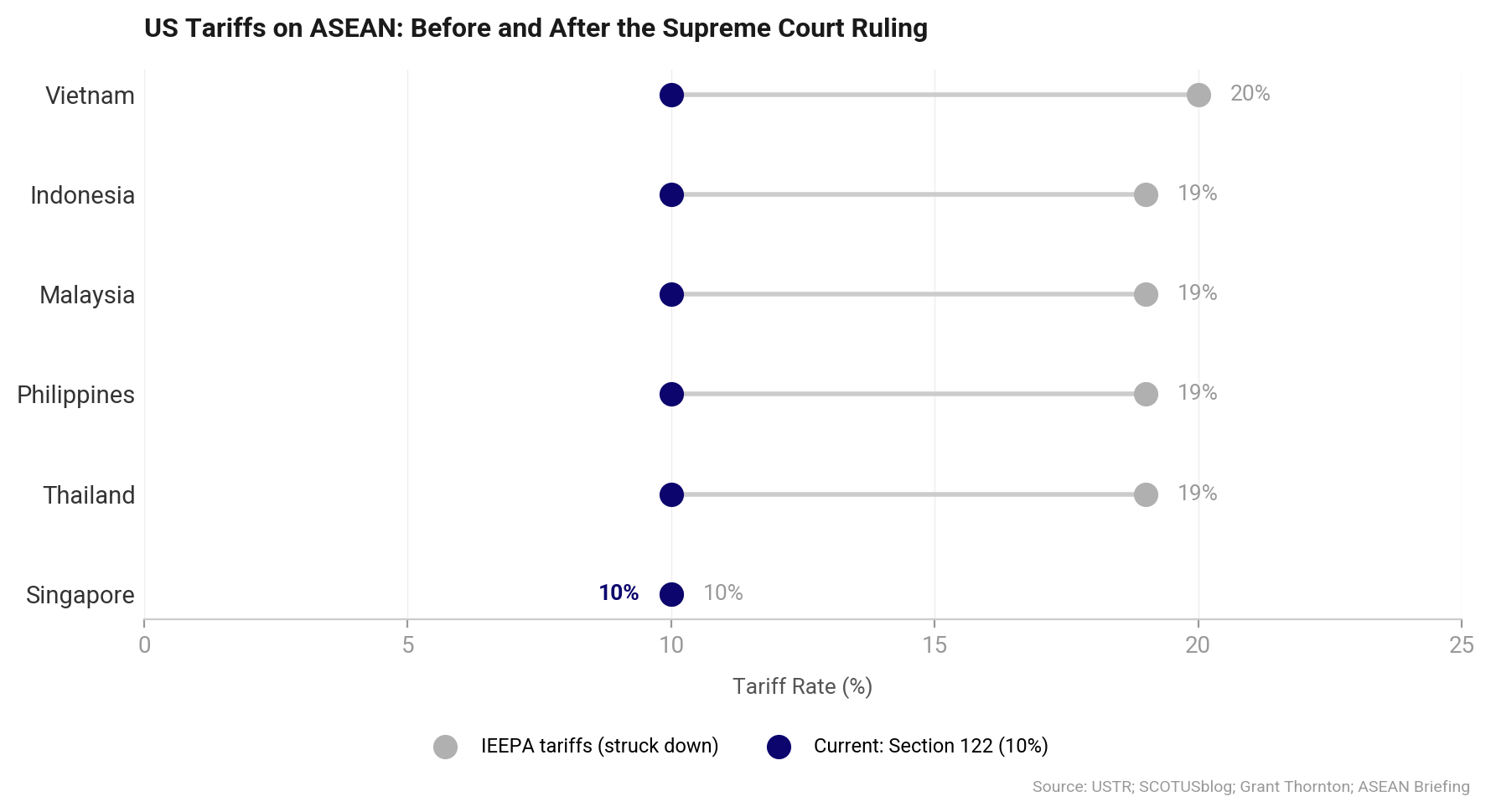

On February 20, 2026, the US Supreme Court ruled 6–3 in Learning Resources Inc. v. Trump that IEEPA does not authorise the President to impose tariffs, striking down the entire reciprocal tariff framework. The decision invalidated approximately $175–179 billion in collected duties.

The administration responded within days. A new 10% global tariff was imposed under Section 122 of the Trade Act. On March 11, USTR Jamieson Greer launched Section 301 investigations against 16 countries, including six ASEAN economies — Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Cambodia — targeting structural excess capacity and manufacturing production practices. These investigations are the precursors to country-specific tariffs, though they take months to conclude.

The result is a tariff landscape that has gone from uniform to fragmented in under six weeks. For businesses with operations across multiple ASEAN markets, this means managing not one tariff regime but several — potentially with different rates, timelines, and legal bases.

Dependency Substitution, Not Diversification

ASEAN’s collective response to trade pressure from the United States has not been retaliation but redirection. Bilateral trade between China and ASEAN grew 9.7% year-on-year in the first eight months of 2025, reaching a record $694 billion. Manufactured goods accounted for over 90% of this trade, with Chinese exports of machine tools and auto parts to ASEAN increasing by 56% and 22% respectively.

This is not diversification. It is dependency substitution. These economies remain intermediaries in a contest between two major powers, with limited leverage over either. The Supreme Court ruling did not resolve this structural exposure — it merely changed the legal mechanism through which it will be tested next.

Capital Arriving Faster Than Institutions Can Absorb

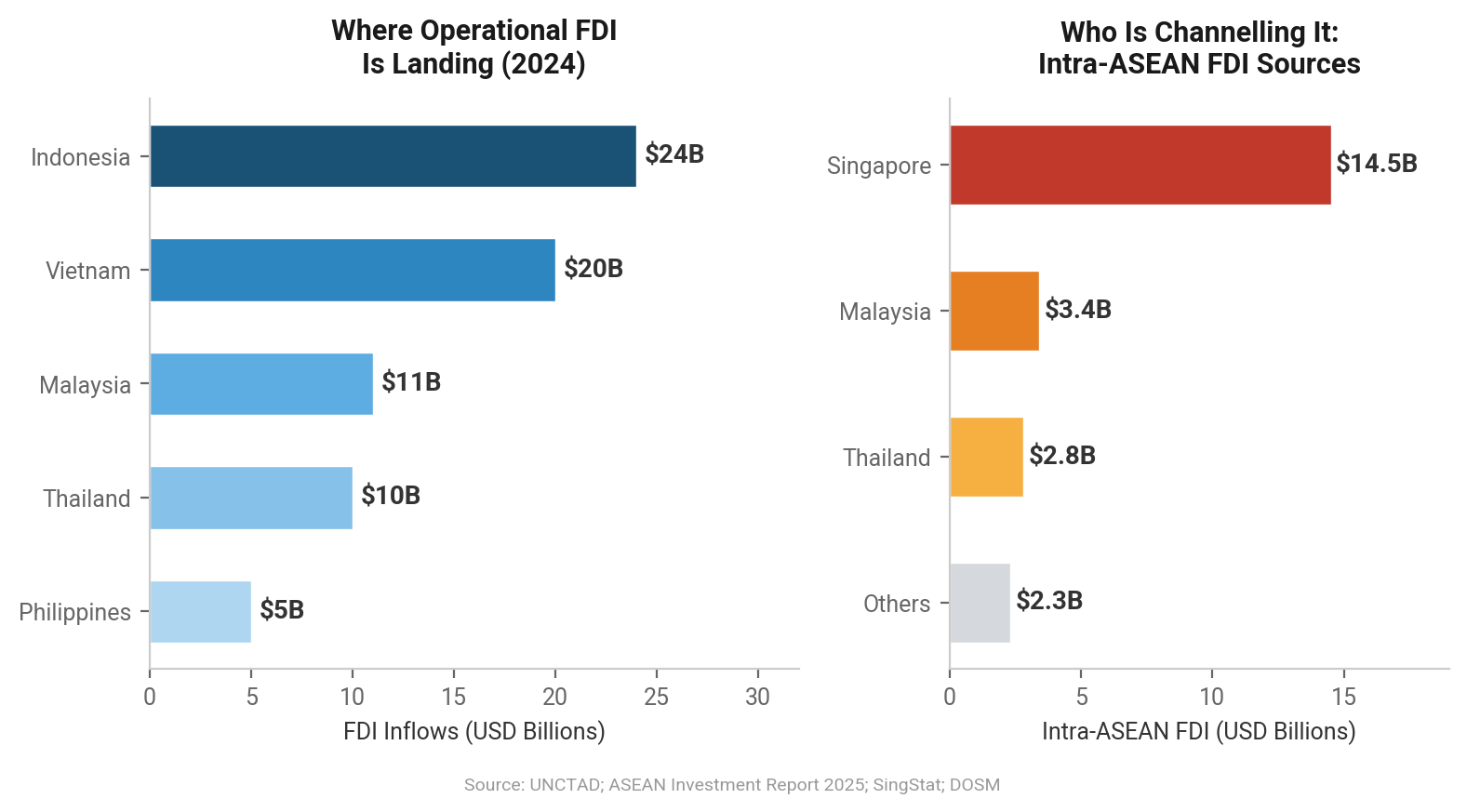

The headline ASEAN FDI figure of $226 billion requires careful disaggregation. Singapore recorded approximately $192 billion in inflows, but functions primarily as a gateway — a regional headquarters and financial conduit through which capital is routed onward. The economies receiving the most operationally significant investment — Indonesia ($24 billion), Vietnam ($20 billion), and Malaysia ($11 billion) — are where factories are being built and supply chains are being physically relocated.

It is in these markets that the gap between capital inflows and institutional capacity is most consequential.

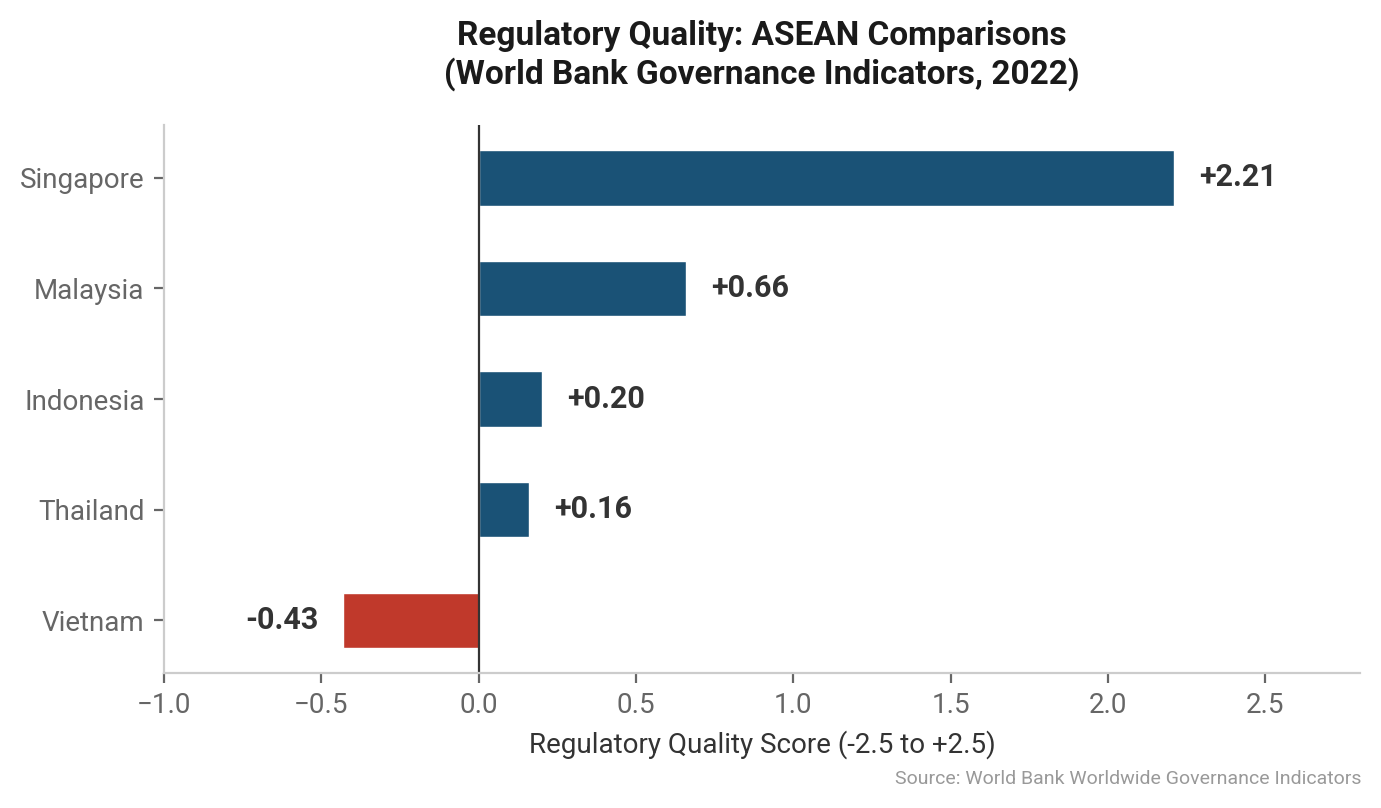

The Regulatory Quality Gap

The World Bank’s Worldwide Governance Indicators provide a quantitative lens on this challenge. On regulatory quality — the ability of a government to formulate and implement sound policies that promote private sector development — the disparities within ASEAN are stark:

• Singapore: +2.21

• Malaysia: +0.66

• Indonesia: +0.20

• Thailand: +0.16

• Vietnam: −0.43

Vietnam’s score places it below zero on a scale from −2.5 to +2.5, indicating a regulatory environment that falls short of the global median. Indonesia, while marginally positive, continues to acknowledge structural bottlenecks in regulatory consistency and sub-national government capacity.

Compounding this is the pace of regulatory change. Malaysia and Thailand have introduced new requirements around data centre development, grid access, and digital platform regulation. Indonesia is pursuing localisation mandates and revisiting foreign ownership thresholds in strategic sectors. For companies that entered these markets under one set of assumptions, the landscape 18 months later may look materially different.

The Risks Boards Are Not Pricing

Taken together, these dynamics create a risk profile that most governance and risk management frameworks are not designed to capture:

• Trade corridor concentration. Vietnam’s US exports equal 30% of GDP. The tariff regime is shifting from IEEPA to Section 122 plus pending Section 301 investigations. Binary exposure to US–China policy shifts, compounded by legal uncertainty around the tariff basis.

• Dependency substitution. China–ASEAN trade up 9.7% in H1 2025, over 90% manufactured goods. Replacing one dependency with another. The diversification narrative may be misleading.

• Regulatory velocity. Vietnam’s regulatory quality score at −0.43, Indonesia at +0.20. Rules are changing during the scaling phase. Point-in-time due diligence is insufficient.

• Operational scaling vs governance capacity. Manufacturing FDI up 150% in one year. Data centre oversight tightening across ASEAN. Rapid expansion in jurisdictions with limited enforcement infrastructure.

None of these risks are individually catastrophic. Their danger lies in their interaction. A company that has concentrated its export operations in Vietnam to serve the US market, relying on Chinese inputs, while scaling facilities under regulatory assumptions that are already shifting, faces a compounding set of vulnerabilities that no single risk metric will flag.

What Good Looks Like

The purpose of this analysis is not to argue against investment in Southeast Asia. The growth opportunity is real, and the region’s structural advantages — demographics, geographic positioning, improving infrastructure — are durable.

The argument is that the governance and strategic resilience required to capture that opportunity are being underinvested relative to the commercial scaling already underway. The boards and investors who recognise this are not pulling back. They are building the institutional capacity to stay.

We see four areas where the gap between commercial ambition and governance readiness is most acute:

• Trade corridor risk. Rolling scenario analysis embedded in board-level risk reporting — not static risk registers reviewed periodically.

• Regulatory trajectory. Continuous monitoring of regulatory direction as a core input to expansion decisions — not point-in-time legal due diligence at market entry.

• Governance infrastructure. Local governance, government relations, and operational controls scaled at the same pace as commercial operations — not compliance bolted on after the fact.

• Stress testing. Structured stress tests asking what happens if tariffs tighten, if a key market introduces localisation mandates, or if China–US tensions escalate — not assumption-based financial models.

These are not abstract recommendations. They reflect the operational reality of advising corporates and investors navigating the region today. The cost of building this resilience is modest relative to the cost of discovering, under pressure, that it was never built.

Conclusion

The connector economy model has delivered extraordinary growth for Southeast Asia. But the same characteristics that make the region attractive — its position between great powers, its openness to capital, its speed of development — are also sources of fragility.

The growth narrative is not wrong. It is incomplete. And in a region where the rules of engagement are being rewritten in real time, an incomplete picture is a dangerous one.

The boards and investors who will succeed in ASEAN over the next decade are not those with the most aggressive expansion plans. They are those who have built the governance, compliance, and strategic flexibility to navigate an environment where the only certainty is that the assumptions of today will not hold tomorrow.