Rehabilitation Year Zero: Vietnam’s New Restructuring Regime

July 2026 | Monthly Insights

Vietnam's new restructuring regime meets an easing property-bond wall and a deepening renewables payment crisis — it can restructure the debts of both, but resolve only one.

Vietnam's Law on Rehabilitation and Bankruptcy took effect on 1 March 2026, replacing a rarely-used, liquidation-focused regime with an early-intervention, debtor-in-possession rescue overseen by a court-appointed administrator. It arrives while Vietnam is still working through the corporate distress that crystallised in the 2022–23 bond-market crisis, and that distress is now taking two very different forms. The strain is not confined to these sectors — bank asset quality is weakening and the export sector faces an unsettled US tariff outlook — but property and renewables test the regime most sharply, at opposite ends of what it can resolve. The property-bond wall, the kind of distress the regime can most readily address, is already easing: third-quarter maturities are down 47% year on year and overdue bonds stand at just 2.3% of the market. The harder problem is a renewables payment crisis, in which the state offtaker has retroactively cut and withheld tariff payments and pushed otherwise solvent producers into default. A rehabilitation regime can restructure the debts of companies in either sector, but it does not restore revenue. For the property sector, where the binding constraint is leverage against a market that can recover, relief on the debt can be enough; for the producers, whose revenue has been cut by the state offtaker, it leaves the cause untouched, and the cure lies in the power-purchase agreement and arbitration rather than in a rehabilitation plan. The regime's first real test will therefore come from the distress it cannot resolve on its own, and creditors and sponsors should diagnose which problem they are holding before they choose a forum.

The Regime Vietnam Just Switched On

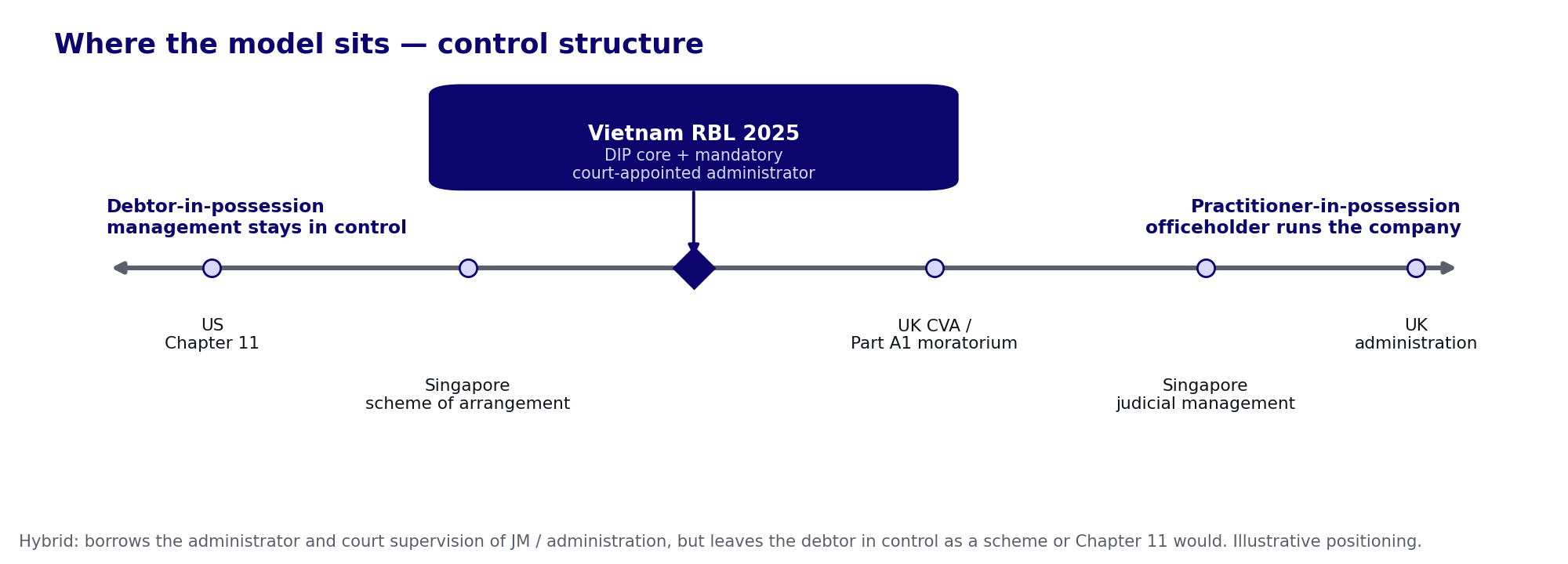

Vietnam adopted a new Law on Rehabilitation and Bankruptcy on 11 December 2025, and it took effect on 1 March 2026, with specialised courts to hear the cases. The framework is a real upgrade. It moves the country away from a liquidation-focused regime that was rarely used and towards an early-intervention, rehabilitation-first model — a debtor-in-possession process overseen by a court-appointed administrator, closer in its control structure to a Singapore scheme of arrangement or US Chapter 11 than to the practitioner-in-possession regimes of judicial management or UK administration, though it borrows the administrator and court supervision from the latter. The natural reading is that Vietnam is catching up with international practice, and on the law itself that reading is correct.

The process is debtor-led. A company may initiate rehabilitation when it faces "imminent insolvency" — broadly, where it expects to be unable to pay debts falling due within the next six months, or has debts overdue by less than six months — rather than only after it has already failed. The debtor retains carriage of the business and prepares the plan, under the supervision of an administrator and a court-formed creditors' committee. Both secured and unsecured creditors vote, and a plan is approved where creditors representing at least 65% of the debt held by those attending the creditors' meeting vote in favour; a reduced threshold of 51% applies to an expedited process for small companies. The plan must then be sanctioned by the court, and the rehabilitation is time-limited. While it runs, the company can obtain temporary relief, including a stay on enforcement against secured assets.

Taken on its own terms, this is a credible piece of law reform. It gives viable but over-leveraged companies a route to reorganise before value has leaked away, and it gives creditors a more predictable process than the ad hoc, out-of-court workouts that have characterised Vietnamese distress to date. The law also introduces, for the first time, provisions for cross-border cooperation, allowing the Vietnamese courts both to seek and to respond to assistance from foreign courts. Two practical gaps matter for the institutions that will use it. First, rescue financing is only lightly provided for: new money raised for the rehabilitation may carry interest, but the law stops short of a clear super-priority or priming-lien regime, leaving the protection and pricing of rescue capital uncertain. Second, several mechanics — the formation of creditor committees, the operation of the enforcement stay, and the cross-border provisions themselves — await Supreme Court guidance, and the regime has no track record.

A further uncertainty sits at the centre of the model. The process is debtor-in-possession in name, but the debtor operates under the supervision of a court-appointed administrator and a court-formed creditors' committee, and the law says little about how far that supervision will reach in practice. It is not yet clear whether the administrator will simply monitor the business and verify claims or will come to direct it, nor how readily the committee — which can ask the court to replace management it considers ineffective — will reach for that power. Until the courts establish how intrusive the oversight becomes, neither side can be sure how much control actually changes hands on filing. A debtor may find the process more intrusive than the debtor-in-possession label suggests, and a creditor may find the committee a softer lever than it expected. That ambiguity is itself a planning problem: the value of the regime to either party turns on how it is administered, which will not be known until the first contested cases are run.

Wave One: The Leverage Problem

Vietnam's distress in 2026 is not confined to two sectors. Bank asset quality is weakening beneath a benign headline — reported non-performing loans are under 2%, but on a broader measure that includes debt parked with the national asset-management company the figure is closer to 6% — while construction tracks the property downturn and exporters face an unsettled US tariff outlook after the prior US tariff regime was struck down in early 2026. Property and renewables are taken here not because they are the only sectors under strain, but because they sit at opposite ends of what a rehabilitation regime can resolve — one a debt problem the law is built to compromise, the other a revenue problem it cannot touch.

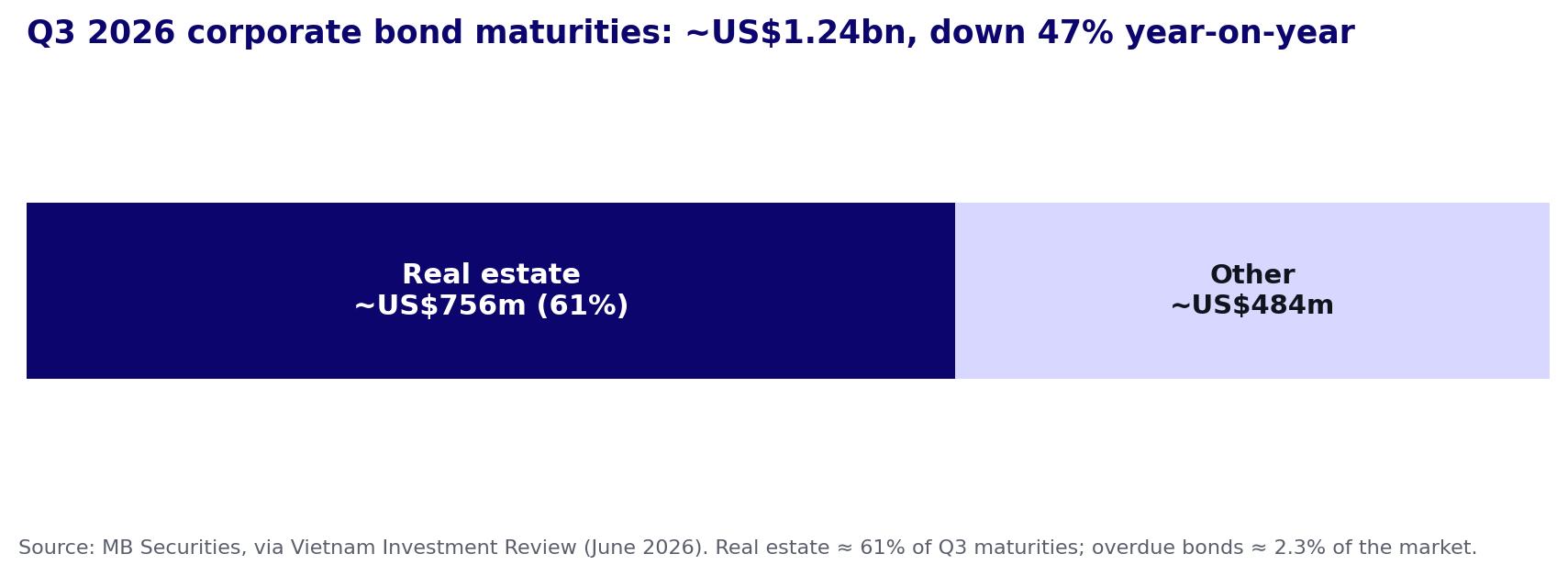

The property-bond wall is the distress the new regime was built for, and on the latest data it is already moderating. On MB Securities' June 2026 estimates, around US$1.24 billion of corporate bonds falls due in the third quarter of 2026, a decline of 47% on the same period a year earlier, and the value of bonds with overdue payment obligations stood at roughly US$1.26 billion at the end of May, equivalent to only 2.3% of the outstanding market. Early redemptions have been heavy: about US$3.26 billion of bonds were bought back in the first five months of the year, up almost a third year on year, pulling future maturities forward and taking pressure off the wall.

Real estate nonetheless remains the centre of gravity. Developers account for roughly 61% of the bonds maturing in the third quarter, about US$756 million, and they continue to pay the highest cost of money, with real-estate bonds priced at a weighted-average coupon of about 12.5% in May, well above the market-wide average of about 9.7%. The redemptions easing the aggregate picture are overwhelmingly a banking-sector phenomenon, with banks representing some 93.7% of May's buybacks, while real-estate redemptions fell more than three-quarters year on year. The deleveraging, in other words, is being done largely by the issuers that were never the concern, while the leveraged developers are refinancing at double-digit coupons rather than retiring debt.

This is conventional balance-sheet distress: developers that borrowed heavily against project portfolios that are slow to monetise, refinancing at high cost as bank credit and new issuance stay disciplined. For this category of borrower the rehabilitation regime is well matched, because the problem is the capital structure and the law is built to restructure a capital structure — binding a dissenting minority through the 65% threshold, holding enforcement at bay while a plan is negotiated, and giving a viable business time to recover. With the aggregate wall already easing, the property wave is the more manageable of the two. The harder test for the new law lies in the second wave, where the distress does not originate in the balance sheet at all.

Wave Two: The Revenue Problem

The second wave is different in kind. Since the January 2025 invoices, EVN has applied a lower, self-proposed tariff to solar and wind projects already in commercial operation, withholding part of the payments due and moving to claw back what it now treats as overpayments. The dispute turns on a construction-completion certificate that EVN says these projects lacked at their commercial-operation date, but which their contracts and the feed-in-tariff rules never required for entitlement; by April 2026 the Ministry of Industry and Trade had proposed retroactive reductions of 25% to 46% across roughly 173 operating projects representing some US$13 billion of investment, a matter that remains unresolved. With revenue cut at source, these producers are breaching covenants to local and international lenders and facing default on monthly debt service. Vietnamese solar power-purchase agreements have already been described by financiers as effectively unbankable.

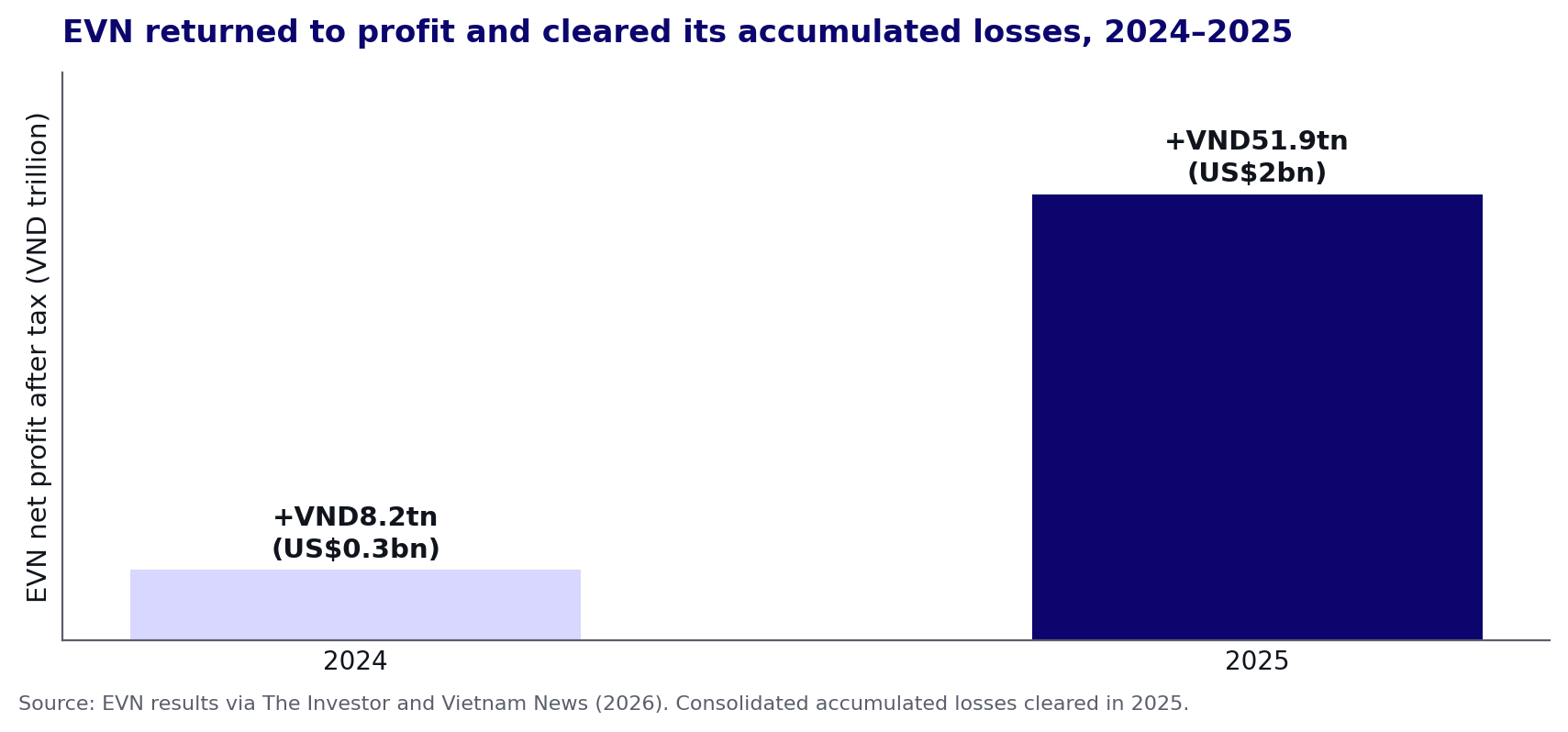

The counterparty's position, if anything, makes the problem starker. EVN returned to profit in 2024 (about VND8.2 trillion, or US$0.3 billion) and posted a far larger profit of about VND51.9 trillion (US$2.0 billion) in 2025, clearing on a consolidated basis the accumulated losses it had carried since the 2022–23 fuel-cost spike. The withholding of payments is therefore not a liquidity failure that a workout could ease; it is a policy and legal stance, with the Ministry of Industry and Trade directing the eligibility review even as the utility's own finances recover. A producer in this position does not have a leverage problem that a rehabilitation plan can solve. It has a revenue problem created by the conduct of a now-solvent, state-owned offtaker — and a rehabilitation statute cannot rewrite the offtake contract or compel the counterparty to honour the original tariff.

There is a clear precedent for where this leads, and a caution within it. When Spain rolled back its solar subsidies between 2010 and 2014, foreign investors took the state to arbitration rather than restructuring their debt and moving on. Tribunals ruled against Spain repeatedly, yet enforcement proved slow and contested: by mid-2025 Spain still faced roughly EUR1.5 billion in unpaid awards, having made only its first payment, of about EUR23.5 million, that June. Foreign-sponsored Vietnamese renewable projects, many financed by international lenders and held through treaty-protected structures, have every incentive to take the same route, and their first recourse is the contract and the treaty rather than the rehabilitation regime.

That is not the end of the regime's relevance. Arbitration is slow, typically running several years to an award and longer to enforcement, while debt service falls due every month against revenue that has already been cut. A producer that has sued cannot simply wait for the outcome; it will often need to use the rehabilitation process in parallel — to stay enforcement, reschedule or compromise its debt, and hold the financing together until the claim resolves. Some will restructure first to stabilise and then litigate; many will run both at once. The regime's role here is to keep the producer and its financing intact until the award arrives, with the recovery itself coming from the arbitration.

Read that way, its limits come into focus. The process is time-limited — early commentary points to a cap of around three years — which may be shorter than the arbitration it is meant to outlast. New money to fund the wait has no clear priority. And a plan needs the support of creditors holding 65% of the debt, who must be willing to treat an uncertain, enforcement-dependent award as the asset that makes the plan work. The sequencing itself has to be managed with care, so that a domestic filing does not prejudice the treaty claim.

Where the Regime Bends

Placed side by side, the two waves expose the limits of even a well-drafted rehabilitation regime. The law can compromise liabilities; it cannot restore revenue. The property sector is not without a revenue problem of its own, since projects are slow to sell, but there the weakness is cyclical, and relief on the debt buys time for a market that can recover. The producers' revenue, by contrast, has been removed by decision, and no amount of time restores it. For the property developers, then, the new process is a plausible venue and may well prove its worth. For the renewable producers, the regime reaches only their debts to their lenders; the dispute that actually matters — over the tariff and the withheld payments — lies between the project and the state, and is resolved through the power-purchase agreement and arbitration, not through a rehabilitation plan — though a rehabilitation may still be needed to carry the producer's financing through the years such a claim takes.

This is the uncomfortable position in which Vietnam finds itself. The reform is genuine, but the harder of the two distress waves sits largely outside what any domestic insolvency law can reach. The renewables cases may therefore test the regime's limits faster than the property cases validate its strengths, and they will do so while the courts are still establishing how the new procedure works in practice — including how its untested cross-border provisions operate and how rescue financing ranks in the absence of a clear super-priority regime — and how any of it interacts with investment-treaty claims. A first cycle that includes disputes the statute cannot resolve is a demanding way to build precedent.

What Good Looks Like

The practical task for lenders, sponsors and investors is to diagnose which problem they are holding before they choose a venue. Leverage distress and revenue distress look similar on a missed-payment notice and call for very different responses. Where the issue is an over-geared but viable operating business, the new rehabilitation process is worth engaging early, while the company still has options and before value erodes; the 65% threshold and the enforcement stay are most useful to a creditor who helps shape the plan rather than one who waits to vote on it. Where the issue is an impaired offtake contract, the claim and the workout belong in one plan. The treaty or arbitration claim is the route to recovery and should be asserted and protected first, while the rehabilitation is used to stay enforcement and restructure the debt so the producer survives until the award. The error is to treat them as alternatives, or to file domestically in a way that weakens the claim.

For investors positioning into Vietnamese distress, the same distinction sets the price. The property wave is a recovery story, to be underwritten on asset value and plan feasibility. The renewables wave is a legal and political-risk story, whose value turns on the strength of the contract and the treaty rather than the balance sheet.

Conclusion

Vietnam has built a modern restructuring regime at the moment it most needs one, and that is to its credit. The regime will resolve the distress that is really about the debt, which is much of the property sector. The harder question is what happens to the distress that is about lost revenue, which it cannot reach, and the parties who answer that question early — by choosing the right forum for the right problem — will preserve options that those who file first and think later will have given away.